The Real Reason Bitcoin Startups Are Struggling to Fundraise

If you’ve read my blog over the years, you know I’ve written extensively on bitcoin in the WSJ, re/code, and Coindesk. And yet, a couple of years after my initial interest in the bitcoin sector, neither myself nor my firm Chicago Ventures is yet to make an investment into a bitcoin tech startup. And that in spite of my taking a large personal stake into bitcoin itself, and many “altcoins” such as Ethereum, Maidsafe and Factom. Let me be clear: I am an unequivocal bitcoin bull. I believe that bitcoin may well represent the greatest transfer of wealth in my generation. I also believe that bitcoin itself, as the fuel underlying the blockchain, is exceedingly vital – as very clearly outlined by my friend Nick Tomaino in The Blockchain is Important and so is Bitcoin.

For the past 12-18 months I have intentionally passed on nearly every early stage bitcoin related business because of what I believe to be a systemic funding gap that is not easily reconcilable. Simply put: given the macro level of consumer adoption within bitcoin (below) it is exceedingly difficult for most new entrants to reach a level of traction compelling enough to warrant follow on capital. And because the majority of these businesses are not generating substantial revenue, availability of continuation capital is a pre-requisite to any current funding round.

So where is consumer adoption of bitcoin? One of the better breakdowns I’ve seen is by Tim Swanson on his blog Of Numbers – where he chops the data multiple ways and finds at best 2x year/year growth: A Brief History of Bitcoin “Wallet” Growth (whereas most VC-backed consumer companies are shooting for 5-10x+ Y/Y growth).

bitcoingap1

EARLY STAGE CONCERNS

My hesitation towards investing in the sector comes from the following analysis (the data behind my analysis, as well as copied graphs are via Coindesk). Here’s the data as I’ve assessed it -

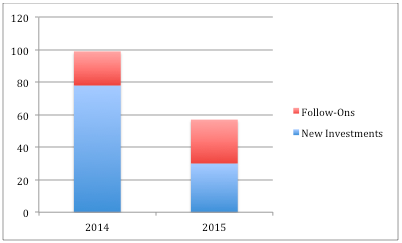

bitcoingap2

2015 saw a nearly 50% decline in total bitcoin related VC deals from 99 to 57. Though that reflects a macro-level hesitancy on the sector (or perhaps over-exuberance in the 2014 bull market), that – in and of itself – is not debilitating.

But the two disconcerting trends to most early stage investors are:

Of the 78 newly funded companies in 2014, only 21 raised follow on funding in 2015 (6 of the 27 follow-on rounds in 2015 were for companies who had first been funded in 2013).

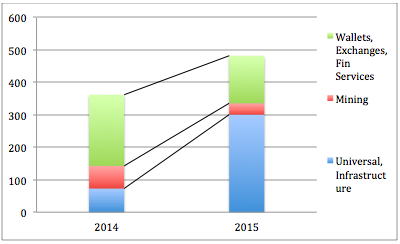

Funding is fast consolidating quickly around “platform” investments (as expressed by the graphs below) – which I characterize as either “universal” or “infrastructure” focused. These are the startups least exposed to the short-term volatility of consumer adoption as they touch multiple parts of the ecosystem.

The evidence appears in these two charts:

bitcoingap3

bitcoingap4

Universal and Infrastructure related investments now make up nearly 50% of all bitcoin funding, but more importantly, are the buckets into which all of the year’s largest funding rounds fell into: Coinbase, $75M (Universal), 21 Inc, $116M (Universal), Circle, $50M (Universal), and Chain $30M (Infrastructure).

With that in mind, let’s unpack those two points –

(1) With 57 of the 78 funded companies in 2014 not raising publicly disclosed follow on funding round in 2015 that means that there are either (a) a lot of likely zombie bitcoin startups or (b) a large number of non-disclosed bridge/extension rounds.

Though bridge rounds are a sub-optimal situation for founders and investors alike, they are a reality and we’ve done our share of them at Chicago Ventures. The problem here is that an extension is fundamentally a “bridge to an outcome” - and in the case of most of these bitcoin startups, neither the market nor macro adoption has converged to the point where a meaningful “outcome” is achievable in 6-18 months.

When investors consider making a new investment in the space, they are increasingly cognizant that bitcoin adoption will not explode overnight and that the funding duration for any consumer-facing company is likely to be 5-10 years before generating material revenue. Given the technical nature of these businesses – and the consequent requirement to staff expert engineers – it’s a very cash intensive proposition to take on and a tough hurdle to overcome.

Nevertheless, of the 30 newly funded startups in 2015, a full two thirds touched payment processing, financial services (transfers) or wallets – the exact categories that are hardest to generate outperformance in the current macro environment.

(2) Over the past two years, much investor commentary has focused on discovering and funding “bitcoin’s killer app.” It is unclear to me whether that was simply a nascent understanding of the ecosystem or intentional misdirection, but it is a misunderstanding. The inherent flaw in that thesis is that it naively assumes that bitcoin is missing a UI, whereas in reality, the blockchain – because it can be leveraged by existing experiences – already has millions of beautiful interfaces to tap into.

Given that, it makes sense that funding is converging around platform plays: those that are either the building blocks of the emerging blockchain ecosystem or those with demonstrable network effects. The struggle for early stage investors wanting to make platform bets is that being a laggard into a space where competitors’ network effects are already strengthening is a recipe for disaster.

Here’s what the funding shift looks like in graphical form as the smart money transitioned towards platform focused opportunities as opposed to discovering a “killer” front-end app.

bitcoingap5

THE NEXT 24 MONTHS

At the time of this writing, bitcoin is once again buzzing: after nearly a year of price decreases and stagnation towards $200, bitcoin has been on a roll, surging past $500 and now holding strong in the mid $400s. In addition, both Wired and Gizmodo believe they’ve uncovered the actual Satoshi Nakamoto, an eccentric, iconoclastic, tax dodging entrepreneur: Australian Dr. Craig Wright, although those who’ve communicated with Satoshi in the past disagree.

It sure does seem likely that 2016 could be another boom year for the broader bitcoin ecosystem.

But the described concerns remain – without a discernable shift in adoption, the vast majority of bitcoin related opportunities, both consumer and b2b blockchain focused, are exceedingly difficult to fund by early stage funds. Consumer, because of largely stagnant adoption, and, b2b, because of the relatively small size of most pilot contracts signed for ledger-focused blockchain-related record keeping. The exceptions, of course, are Barry Silbert’s Digital Currency Group and Dan Morehead’s Pantera Capital, both of whom are committed to expanding the overall bitcoin ecosystem via early stage bets.

Naturally, this equation is also different for larger funds that are opportunistically investing downstream for the right entrepreneur or idea – in that case, they have the pockets to support a company throughout the funding gap. But that is the exception rather than the norm.

My estimation is that smart money at the early stage will largely stay on the sidelines in 2016, waiting to see if new platform opportunities emerge via the 21 Bitcoin Computer, or other decentralized networks, especially as incumbents such as Coinbase, Circle and Chain prove the strength in their networks and multi-faceted applicability.