Why Amazon Has Consumer Investors Bemused and Confused

Amazon’s recent entries into home services, food delivery, private label clothes & shoes, as well as a wide range of private label home items represent its most brazen efforts ever to attack the entire retail stack as well as penetrate seemingly defensible network effect businesses. Over the past couple of years, Chicago Ventures has made a number of investments in service-enabled (concierge) commerce businesses believing that their service layer provides a real defensibility against Amazon’s low (no) margin approach. Writing in TechCrunch this past December in “The Middleman Strikes Back,” I noted then:

“If you sell practically any physical good online, Amazon, the Internet’s most powerful retailer, is a perpetual threat. With their distribution, leverage and logistics expertise, they have the wherewithal to undercut on price, and process and deliver products faster than practically any startup — not to mention, they can operate at a loss if necessary.

So where is Amazon exposed? On a services level.

Amazon’s operating margins — already tight at 1.3 percent — don’t allow for much room to train and mobilize a large human concierge force. Which means that building a human-focused, relationship-driven personalization platform actually provides for a tangible differentiator against Amazon — one of the few ways to effectively compete against the giant (and, perhaps more importantly, one of the few ways to build defensibility in a commerce segment traditionally dependent on “brand” as its only de facto moat).

One further point: Amazon is predominantly a destination for directed search – either on a specific product or specific category basis. But as purchasing increasingly shifts to mobile, it turns out that it continues to be difficult to search, discover and catalogue individual items. Concierges – especially when leveraged via a mobile interaction point – reduce that friction and enable a new purchasing behavior.”

But outside of these concierge commerce businesses – which by the very nature of their human capital costs will inherently be lower margin businesses[1] - are there still opportunities to build consumer businesses in a world increasingly dominated (or potentially undercut) by Amazon?

At an event today in Chicago, Amazon employees from nearby fulfillment centers packed 2,000 care packages to send to soldiers abroad who are not able to come home for the holidays Friday, December 4, 2015. Since 2010, Amazon has shipped more than 12 million packages to APO and FPO addresses. The Amazon care packages for the troops included holiday chocolates and snacks alongside an Amazon Fire tablet. The care packages for soldiers headed off in an Amazon branded trailer—one of thousands that Amazon has started to roll-out to increase capacity in the supply chain. Amazon’s Vice President of North America Operations Mike Roth said, “I couldn’t be more pleased that our very first Amazon trailer headed out on the road carrying such special packages—thousands of boxes filled with beloved holiday items and Amazon Fire devices to support troops abroad this holiday season. (Photo by Peter Wynn Thompson/AP Images for Amazon)

Although many investors and operators I’ve asked privately have expressed mostly bemusement or skepticism about Amazon’s recent efforts, I’ll admit that Amazon has me perpetually on edge.

On Brand Authenticity

On a recent swing through the West Coast I asked several experienced e-commerce entrepreneurs (generated hundreds of millions in annual revenue, raised hundreds of millions of dollars from bulge bracket VC firms) the Amazon question.

The responses were similar: that it is fundamentally unlikely for Amazon to win a branding war in many product categories. For example, one founder noted, Proctor & Gamble or Johnson & Johnson, both of whom are seeing many of their product categories be unbundled by startups, lack the credibility to build authentic new brands in today’s social and content based environments.

How can a corporation claim to represent certain values as underpinning its products when its entire history of operations has been largely antithetical to those same values? Consumers, he argued, are simply too well informed now to be tricked by that ruse.

That strikes me as true – in certain categories. Here’s my view on how many product categories break down from a consumer’s perspective on importance. For context, I believe that purchasing decisions primarily hinge on four variables: Recall Impact is the speed at which a name brand is immediately recognized by a consumer, Authenticity Impact is the natural fit between company (or founders) and its product and messaging, while Review Impact refers to the import of 3rd party or peer-to-peer product reviews.

AmazonConfused4

The takeaway is that authenticity matters – but not always. Bargain shoppers are focused less on company values and story and a lot more on trusted brands who will provide a consistent quality of product at a low price point. Whereas mid-tier buyers care a lot less about traditional household brand names and base far more of their purchasing on crowd sourced information and reviews. This trend is more eloquently described by Itamar Simonson, a Professor at Stanford GSB who argues that we’ve reached “the decline of consumer irrationality,” that is, a large segment of consumers are less malleable to high level branding than in the past.

Amazon’s platform allows it to potentially excel within reviews, recall and price. Reviews, because it has habituated its customers to checking peer reviews before purchasing (and if its products warrant positive reviews, consumers will take note), and Recall, because the Amazon name is effectively ubiquitous with quality and convenience.

What this means is that Amazon has a very credible case to steal market share from bargain brands and mid-tier brands, but will face resistance as it moves into categories where authenticity matters a lot or if its product is subpar, irrespective of price. This is likely why its AmazonBasics line has fared well (low cost, commodity products, mostly electronics), whereas its initial line of diapers was pulled from the market. I am personally suspect that its forthcoming “Mama Bear” line of baby products and organics will be successful

On Irrationality and Execution

As an investor, my job is to pick and help businesses that I believe can execute on models that are defensible and sustainable. But Amazon has shown an unwillingness to accept any network effect as impenetrable and a preference for building, rather than acquiring.

That said, the questions I wanted to unpack are: (a) Is Amazon likely to out-execute a focused, fast growing startup and (b) Are they rational?

Let’s start with (b) – are they rational? I asked a respected consultant to the Fortune500 on strategy and corporate development with deep experience in retail. His thoughts:

“Amazon has always had a very unusual way to do strategy, breaking many of our rules. But along the way, they have also proved that it is a very bad idea to do that. How do I know that? Look at the profit margin per sales dollar, the profit margin per employee, and simply the lack of net profit over the many years. They are masters at "trading dollars" rather than making money. Until very recently, profits have been essentially zero. Never before in history has a major retailer grown without making buckets of money all along the way.

Along the way, to provide the appearance of dynamic growth, they have aggressively been crashing into markets and selling things at or below their real cost (including all true costs of operations). How do I know that? They make no money in the end, and that shows me their true costs, which they work very hard to hide in the individual business sectors.

Amazon does appear to act irrationally, and it is only the superior irrationality of the stock market that allows them to have the capital to do that. Can the profit from AWS actually support the entire enterprise? I have no idea. But I would not want to compete with Amazon in any product space.”

Irrespective of whether one is an Amazon bull or bear (and I think it’s important to learn Chamath Palihapitiya’s take on the bull case) it does appear that their actions in any given business unit are highly experimental, to the point of appearing irrational (though employees will tell you Amazon is extraordinarily data driven). As an operating business, they are either fools or geniuses – both of which are reasonable perspectives – but many of their business launches do appear irrational. For example, Handmade, a direct Etsy competitor announced more than a year ago, has yet to launch and seems an odd market to attack given that Etsy’s market cap at $1.1B, or 33bps of Amazon’s, is downright immaterial.

The second question worth exploring is whether Amazon is likely to out-execute a more nimble startup. Amazon’s past is riddled with failures such as the Fire phone, Amazon Local (its investment in Living Social was also unsuccessful), and others. Whereas its successes, led by Amazon Web Services, Prime, and Echo are undeniably game changing. The reality, like most of life is likely grey – that Amazon’s outliers are outnumbered by its hundreds of somewhat successful experiments

Insights From Public Markets

To date, Amazon’s aggressive low cost pricing and capex-intensive logistic arsenal has most visibly punished traditional brick & mortar retailers. Sears, Macy’s, Nordstrom, Williams-Sonoma, Kohl’s and others have all lagged the S&P 500, often precipitously, for more than five years. In the following two graphs, the S&P 500 is the blue line.

AmazonConfused6

AmazonConfused5

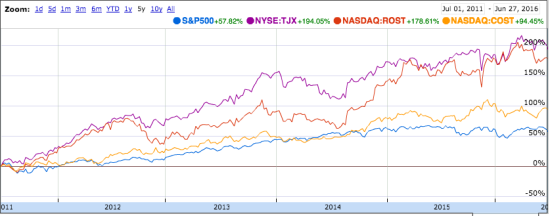

But there’s one glaring exception (in the second graph). Off-price retailers, led by TJ Maxx & Ross Stores have surged, doubling the return of the S&P500 over the same period, and trading at multiples double to triple those of traditional retailers:

AmazonConfused7

In fact, the three brick & mortar retailers with the highest multiples: TJ Maxx, Ross Stores and Michael’s share one unique characteristic: they have effectively zero e-commerce. In fact, the retailer with the next highest multiple is Costco – who do not rank in SEO and whose e-commerce gated and exclusive to annual members.

So what’s the logic? Has Wall Street simply lost its mind & just hates online shoppers?

No. Each of the retailers in the high multiple bucket shares a commonality: a perception of being Amazon-proof. Off-price retailers have a particularly complex business model: frequently changing merchandise, material inventory differences on a store-by-store and geographic basis [3], and opaque relationships with the brands themselves. Those are complexities that are difficult to productize online because of the fast changing nature of the inventory – and for the time being the street assigns a premium to that non-commoditized revenue. [4]

The same is true of both Costco and Michaels. Costco, historically, has enjoyed a structural moat against other retailers because of its membership club and unique approach to high volume/bulk items. That, of course, may be changing – sales were flat for the first time in six years in the last quarter – and it’s possible that slowdown is related to Amazon’s Subscribe & Save. Michael’s stores, the behemoth craft superstore also trades at a material premium to most retailers, presumably because of a combination of (a) its custom framing business, a major revenue driver, has been reluctant to transition online and (b) over 50% of the store’s product revenue comes from private label brands, insulating itself from selling purely commoditized supplies.

High level – these are the insights investors and entrepreneurs should be focusing on when innovating in direct to consumer businesses. With an effectively infinite war-chest and a fearless leader, Amazon’s willingness to compete, even with mid-cap companies such as Etsy and Grubhub is unprecedented and its potential impact, significant. Those insights suggest a focus on building deeply authentic products, innovating in product mixes that are not naturally leveraged by Amazon’s existing logistics, and/or focusing on defensible transactional network effects businesses[5] – while avoiding mid-tier, commoditized product tiers or businesses that compete on logistics.

[1] There may be exceptions. There’s a reason Stitchfix has been investing heavily in data science,reportedlyemploying 60 FT data scientists. Data, even if only partially automated, is they key to reducing these concierge related overhead costs.[2]

[2] The paradoxical element of it all is that if a concierge commerce business (such as Stitchfix) becomes a purely data/AI personalized retailer, then they have unknowingly just played into some of Amazon’s greatest strengths: data leveraged personalization. It would seem there is a balance to be struck in this cycle.

[3] As an aside, one of the amusing nuances of the off-price retailers is that because of their changing inventory, and store-to-store inventory differences, each visit provides a sense of surprise and often delight - that same “surprise” many of the e-commerce based curators have tried to recreate online with mixed success. Turns out you could’ve just walked into an off-price store all this time!

[4] This is also why I am personally intrigued by the online consignment players.TheRealRealfor example has enormous operational complexity because of the one off nature of its inventory – and forced to streamline processing costs (photography, content, authenticity verification, tagging) to the point of being profitable even on $100 items. Our investment inLuxury Garage Saletakes this complexity even further: moving thousands of truly unique SKUs across the country to its different retail stores, and even further re-leveraging the consigned items by putting them in try on at home and return boxes, calledLuxbox.

[5] Grubhub’s network effects, though strong from a technical perspective, are arguably weaker as consumer behavior shifts towards expecting a holistic delivery experience. This is because the company at present does not fully control that experience. Amazon, by virtue of its logistical prowess, can begin to recast the network in its favor, especially if it is willing to undercut on price and subsidize the costs of speed. Whether that is cost effective for them is irrelevant – Amazon is not concerned with short term profits.